I discussed my model long-term all-stocks portfolio in a

post written earlier this month. I’ve decided to revisit this portfolio and add monthly updates pertaining to the performance of this hypothetical portfolio.

My assumptions regarding this portfolio are as follows:

(1) $100,000 was invested on December 31, 2005 according to the approximate percentages of the model portfolio listed in my earlier post;

(2) only whole shares may be purchased of any ETFs or closed-end funds;

(3) partial shares may be purchased for any of the mutual funds;

(4) all ETF and closed-end purchases are made through Ameritrade’s

Izone service, at a cost of $5 per trade;

(5) all distributions for the mutual funds are reinvested; and

(6) all distributions for the ETFs and closed-end funds are placed in a money-market fund (to simplify the calculations, I will assume that the money-market fund does not pay interest).

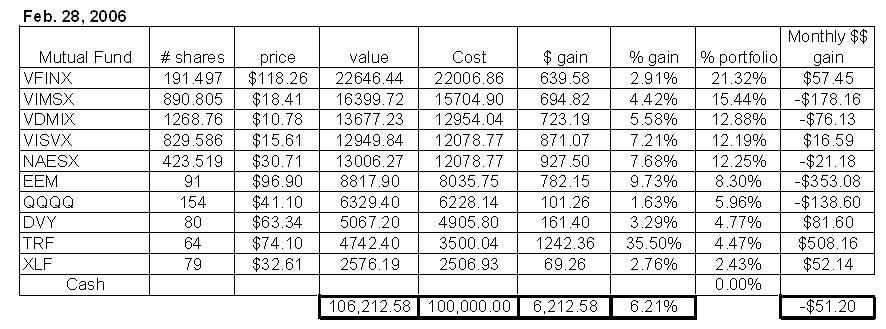

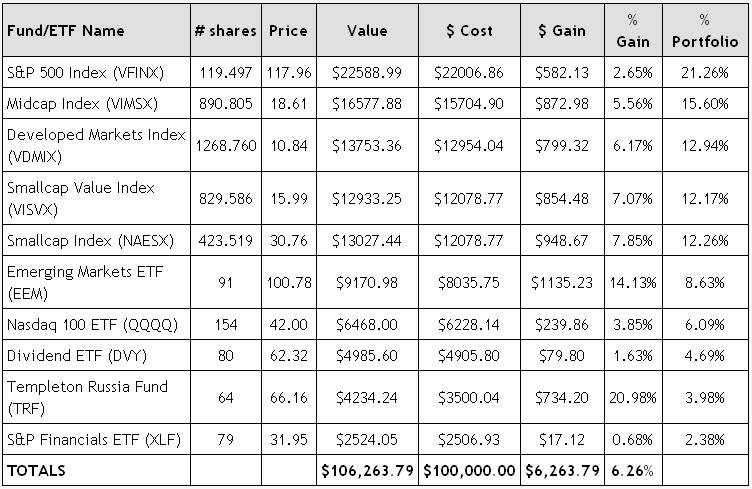

Based on the December 31, 2005 closing prices, the following securities were purchased for the model portfolio:

191.497 shares of VFINX at $114.92, a total cost of $22006.84

890.805 shares of VIMSX at $17.63, a total cost of $15704.90

1268.760 shares of VDIMX at $10.21, a total cost of $12954.04

829.586 shares of VISVX at $14.56, a total cost of $12078.77

423.519 shares of NAESX at $28.52, a total cost of $12078.77

91 shares of EEM at $88.25 plus a $5 commission, a total cost of $8035.75

154 shares of QQQQ at $40.41 plus a $5 commission, a total cost of $6228.14

80 shares of DVY at $61.26 plus a $5 commission, a total cost of $4905.80

64 shares of TRF at $54.61 plus a $5 commission, a total cost of $3500.04

79 shares of XLF at $31.67 plus a $5 commission, a total cost of $2506.93